Biz Home

Views Home

News

Featured

Eco

About

Books

Business

Finance

Investments

Predictions

Country

USA

Germany

Contact Us

TheBizSense Views

Business Viewpoints and Forecasting

Submit Press Release

Menu

Biz Home

Views Home

News

Featured

Eco

About

Books

Business

Finance

Investments

Predictions

Country

USA

Germany

Contact Us

Tag:

Finance

448

Featured

By

bizadmin

Sep 18, 2013

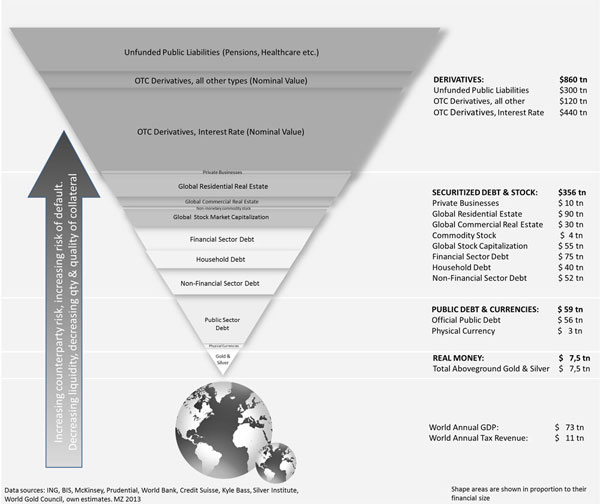

The Global Mountain of Debt

189

Featured

By

bizadmin

Feb 03, 2011

The problem of bloated giants

172

Business

By

bizadmin

Oct 13, 2010

Germany Faces the Burden of Empire